Mergers & Acquisitions | 2016 Year-End Review

- Published: January 25, 2017, By Bill Hornell, Mesirow Financial

For sellers of packaging businesses, 2016 was an excellent year—and the outlook is bright, reports Mesirow Financial.

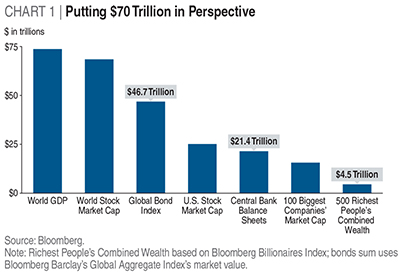

The total market capitalization of all stock markets around the globe currently hovers at around $70 trillion (see Chart 1). This compares to a total global market capitalization of approximately $30 trillion in 2009. It has been the near steady growth of public market capitalizations over the last several years that has been a significant driver of the current merger and acquisition (M&A) boom.

CEOs of public companies are ultimately judged on share price performance, and this healthy stock market environment has rewarded CEOs who have successfully executed M&A strategies to achieve growth. The packaging industry in particular is replete with public companies that have skillfully used M&A as a growth strategy—including WestRock, International Paper, Amcor, Bemis, Transcontinental, Packaging Corp. of America, Berry Plastics, Graphic Packaging, Multi Packaging Solutions, and RPC Group, among others.

Chart 1 also highlights several risk factors that exist in the current economic landscape. Global debt is shown at $47 trillion, but this value includes only publicly traded debt. The International Monetary Fund estimates that total worldwide debt is closer to $150 trillion, approximately twice the level of worldwide GDP. In addition, central bank balance sheets now exceed $20 trillion. Accommodating monetary policies have certainly lowered interest rates, moderated the burden of global debt, and helped boost M&A activity. Presumably though, everything has a limit.

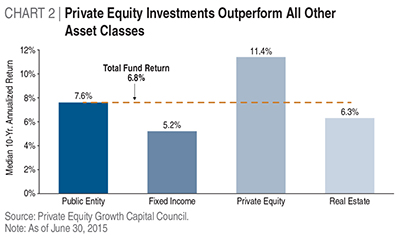

One final point to be made from Chart 1 is that the increasing value of public stock markets has also positively influenced the private equity world. Institutional investors that have seen their overall portfolios rise in value continue to allocate funds into private equity due to its superior performance. In fact, Chart 2 points out that private equity has outperformed other major asset classes.

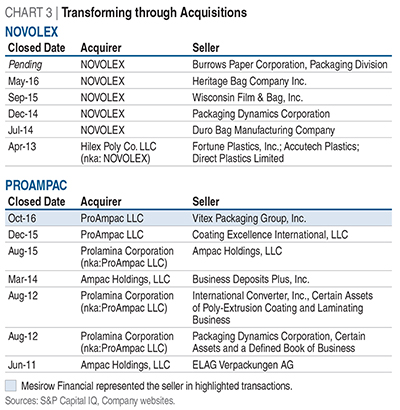

There were two very notable, publicly announced private equity transactions in packaging this year—ProAmpac was sold to the Pritzker Group, and Novolex was sold to the Carlyle Group. Chart 3 shows significant recent acquisitions made by both companies. In four short years, under the ownership of Wind Point Partners in Chicago, Novolex transformed itself from a $500 million in revenue plastic bag manufacturer into a $2 billion specialty packaging business. The company was acquired by Carlyle, a $13 billion private equity fund that will likely continue to pursue acquisitions in specialty packaging. ProAmpac, with the backing of Wellspring Capital, built itself into an estimated $1 billion flexible packaging business. The Pritzker Group is a Chicago-based family office that is also quite active in the packaging industry. Both of these success stories undoubtedly created significant value for the respective company owners. The case studies are emblematic of the private equity opportunities that currently exist in packaging.

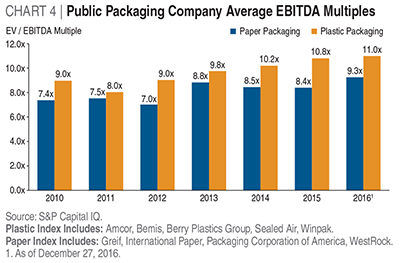

The impact of increasing public company valuations in the packaging industry is shown in Chart 4. These lofty valuation levels are obviously a reward for a job well done (the carrot), but they also set an expectation for future growth that can be difficult to achieve in a low-growth world (the stick). This environment clearly contributes to a focus on strategic M&A to meet growth objectives.

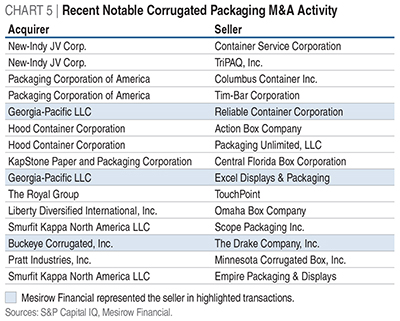

The corrugated industry in 2016 provided an excellent example of using M&A to accomplish corporate goals. Chart 5 highlights several of the numerous corrugated acquisitions that were completed in 2016. Over the last several years, the industry has effectively utilized M&A to improve industry structure and boost industry performance, all amidst a low-growth environment.

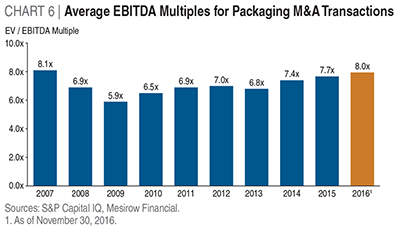

For sellers of packaging businesses, 2016 was an excellent year. Chart 6 indicates that valuations for packaging M&A transactions reached a level not seen since before the financial crisis. It was not uncommon to see double-digit EBITDA multiples paid for large, growing packaging businesses. Part of the valuation story is of course interest rates. Lowered interest rates have lowered rate of return expectations across all asset classes—fixed income, equities, real estate, and private equity. As rate of return expectations come down, valuations and prices move up, and ultimately sellers benefit.

Outlook for 2017

It is difficult to imagine a better environment for M&A than we are experiencing right now. All major factors—interest rates, debt environments, public stock valuations, private equity dry powder, and general economic conditions—are signaling green lights.

We expect continued growth in institutional allocations toward private equity, and packaging will undoubtedly remain a favored industry from the perspective of private equity investors. Strategic buyers will continue their proven ability to create value with well-executed packaging M&A. Finally, it appears that tax rates might move down as well. A strong environment for sellers, indeed.

About the Author

Bill Hornell is a managing director in the Investment Bank Group at Mesirow Financial, Chicago, IL. He has completed more than 100 packaging merger and acquisition transactions. A significant number of these transactions involved consumer packaging businesses. Contact him at 312-595-6196 or at This email address is being protected from spambots. You need JavaScript enabled to view it..